MUMBAI: File progress in gold loans sanctioned by banks and non-banking finance firms is seen to be the set off for RBI to step in and ask lenders to repair gaps in accounting for these loans to keep away from a build-up of unhealthy debt on their books.

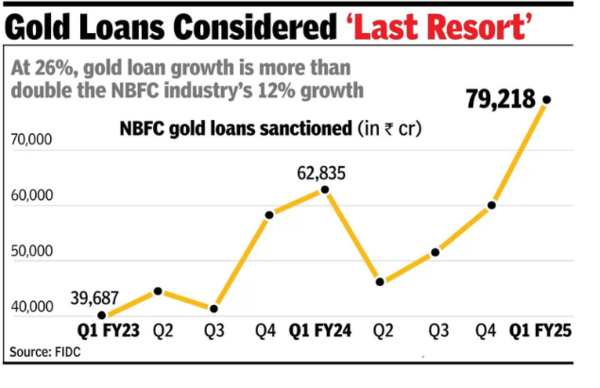

Gold mortgage sanctions in Q1 FY25 grew 26% year-on-year and 32% over the March quarter, with the whole sanctioned quantity equalling Rs 79,217 crore, information by the Finance Business Growth Council confirmed.The rise will not be a one-time prevalence however has been constant over a number of quarters. Throughout April-June 2023, the rise was 10%.

This improve is regardless of stiff competitors from banks within the section. Based on RBI’s sectoral information on financial institution credit score for Aug 2024, gold loans grew almost 41% year-on-year to Rs 1.4 lakh crore.

On Monday, RBI had directed banks and finance firms to evaluate their gold mortgage insurance policies and procedures, and to rectify any deficiencies inside three months’ time. This adopted a evaluate that uncovered irregular practices equivalent to hiding unhealthy loans in addition to evergreening loans by means of top-ups and roll-overs with out correct appraisal.

Whereas gold loans are straightforward to entry, given the collateral, they’re handled because the final resort borrowing by those that unable to faucet into different sources of funding.

The expansion in gold loans is greater than double the general NBFC business’s progress, which noticed mortgage progress of 12% year-on-year. Different segments which have grown at a excessive fee are loans for brand new and used vehicles. The subsequent largest section by way of sanctions is private loans, which account for 14% of NBFC lending. That is adopted by residence loans that are 10% of business loans. Property loans and unsecured enterprise loans stand at somewhat over 8%.