Information from current surveys reveals that the situations we’ve been placing forth all through 2024 proceed to be in play. Particularly, we cite three fundamental dynamics affecting the tech spending local weather, together with: 1) Data know-how budgets proceed to be constrained as; 2) Generative synthetic intelligence is being funded by stealing from different finances buckets; and three) The return on funding for AI initiatives stays tepid, as expectations for break even proceed to be pushed out to the appropriate.

Nonetheless, clients stay extremely optimistic in regards to the prospects for AI driving productiveness enhancements. Furthermore, the cloud stays a key ingredient in supporting AI workloads.

On this Breaking Evaluation, we replace you on the macro spending image in IT, and we’ll revisit the gen AI impression on that spending with some recent survey information from Enterprise Expertise Analysis. We’ll additionally study buyer expectations round cloud workload allocation and particularly have a look at the cloud and its function in supporting AI initiatives.

IT spending stays constricted by uncertainty and the dilutive results of AI funding

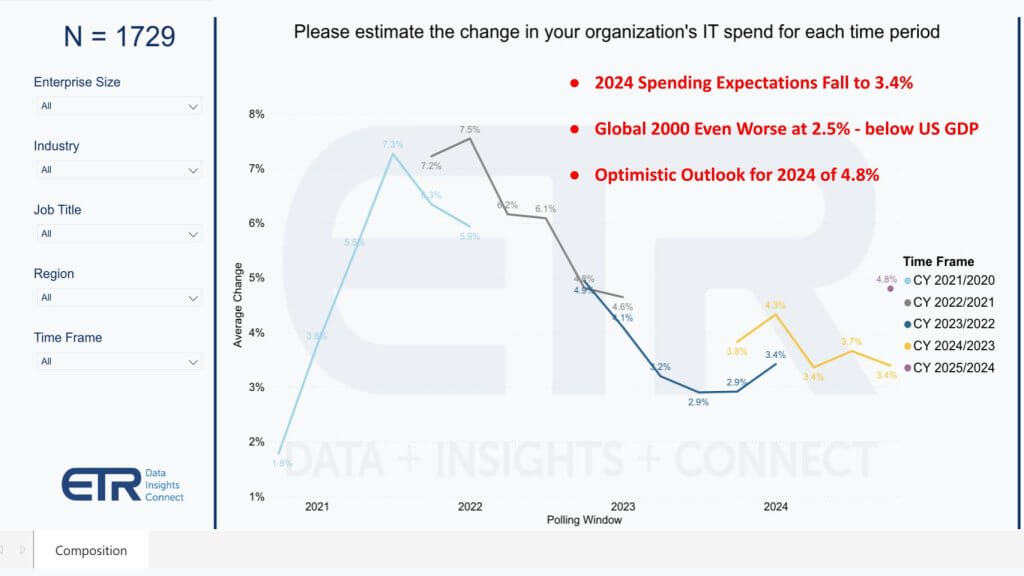

Within the chart beneath, we present the anticipated annual IT spending progress charges for a given yr over time. ETR’s newest macro drill-down survey polls 1,729 IT determination makers. For those who go all the way in which again to the COVID period, we exited 2021 with a really optimistic 7.5% enhance in expectations for top-line IT spending progress in 2022. The battle in Ukraine, Fed tightening and aggressive spending throughout COVID brought about expectations to steadily decline till the Fed stopped tightening in late 2023.

Coming in 2024, we see a reversal, however that was back-loaded. We are able to see above, earlier on this yr IT decision-makers anticipated a 4.3% enhance for the yr. That truly dropped down to three.4% within the spring survey, then turned extra optimistic in the summertime and bumped as much as 3. 7%. This newest survey reveals expectations are again down now to three.4%. Notably, within the World 2000 the expectations are even worse at 2. 5%, which is beneath current GDP forecasts. Regardless of the variability in expectations, IT spending total stays range-bound.

Our assertion is a part of the constraint comes from the truth that AI initiatives are nonetheless not self-funding and are constricting budgets as many organizations are funding AI initiatives by stealing from different budgets. We’ll share information on that in a second.

Vendor consolidation is again in play however laborious to attain

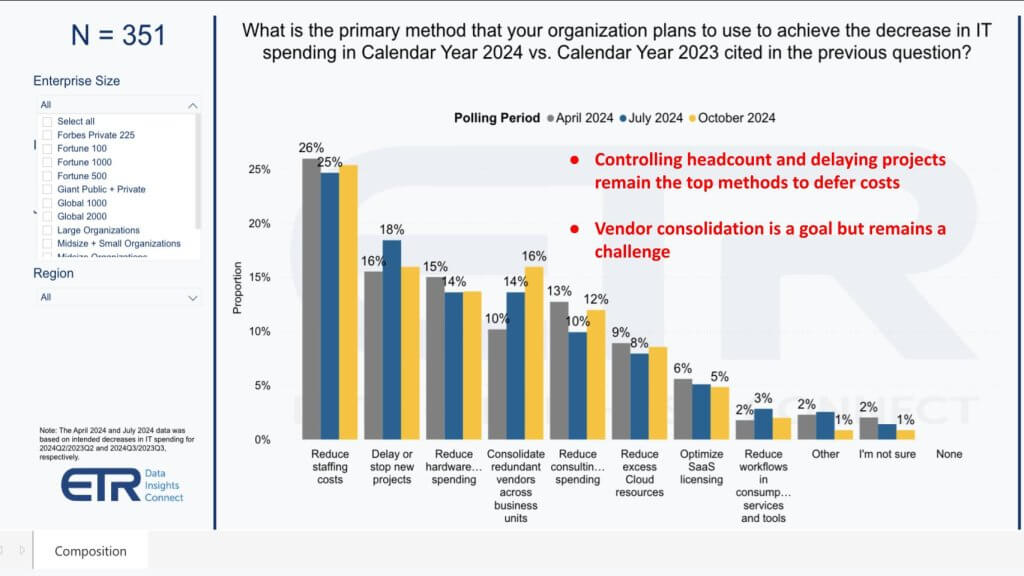

Let’s check out the subsequent information level beneath that reveals us how individuals are fascinated by saving cash. ETR asks: What’s the first methodology that your group is utilizing to attain a lower in IT spending this yr versus final yr?

You possibly can see above that controlling headcount and delaying initiatives are the highest two strategies to defer prices, then {hardware} spending cuts. However vendor consolidation actually popped up right here. You possibly can see it was 10% within the April 2024 survey, so it was pretty benign again then, however now it’s as much as 16%.

Although vendor consolidation is a objective, as we’ve reported, significantly within the cybersecurity sector, it’s troublesome for organizations to consolidate instruments, merchandise and distributors. For example, previous to the RSA Convention, ETR surveys confirmed that solely 9% of the shoppers in that pattern have been efficiently lowering their vendor rely of their safety stacks. So we’re seeing a rise in that technique, however we’ll see if in truth it involves fruition.

AI continues to be diluting different IT spending classes

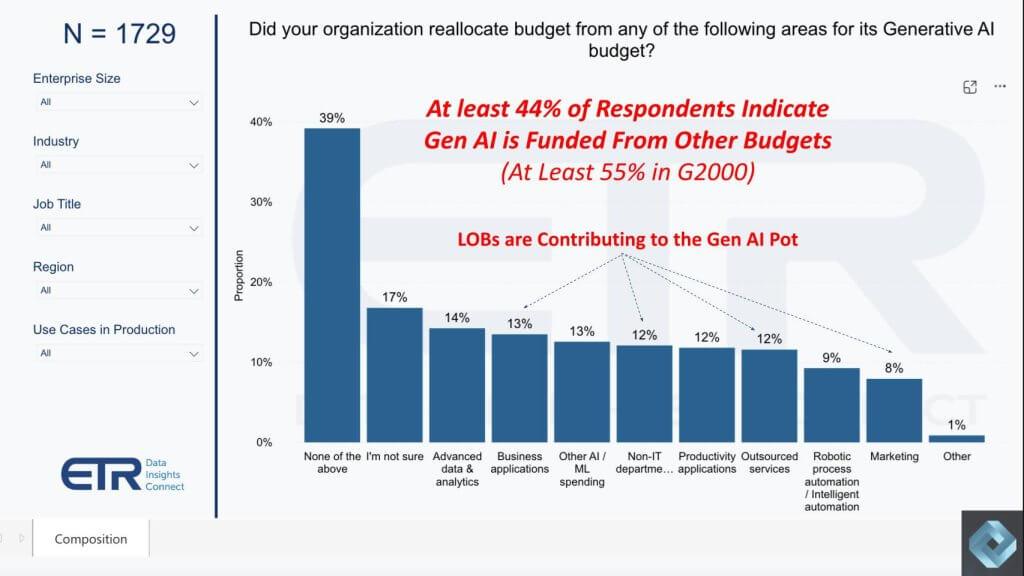

Under we present one of many main components affecting the general macro. On this survey of greater than 1,700 IT determination makers, ETR asks: Did your group reallocate finances from any of the next areas for its gen AI finances?

As we present above in purple, at the least 44% of the respondents point out that gen AI is funded by stealing from different budgets. We’ve seen that quantity hover round 40% to 42% in earlier surveys, and it pops as much as at the least 55% within the World 2000. The rationale why we are saying “at the least” is as a result of we took Not one of the Above and added the Not Certain respondents collectively. So the share of consumers stealing from different budgets to fund AI might be a lot larger – maybe over 60%.

Strains of enterprise are chipping in for AI initiatives

The opposite fascinating new information level proven above is that the traces of enterprise are contributing to that gen AI spend. You possibly can see enterprise purposes at 13%, non- IT departments 12%, outsourced providers at 12%, after which advertising and marketing departments at 8%. So these budgets are coming from different locations and the traces of enterprise have pores and skin within the sport.

The implication is that AI investments are going to have to begin throwing off optimistic money circulate or enterprise line managers will likely be underneath stress. That stress will ripple by the group and trigger a possible backlash. The fact is the super-high-value AI initiatives will take many extra months and even years to pay tremendous giant dividends at most corporations. Although know-how progresses shortly, organizations’ capability to soak up it broadly isn’t trivial. As such, the macro image gained’t see the results of AI for 12 to 18 months at the least and there might be some ache within the meantime.

Most organizations spend lower than $500,000 on AI yearly however large spenders skew the information

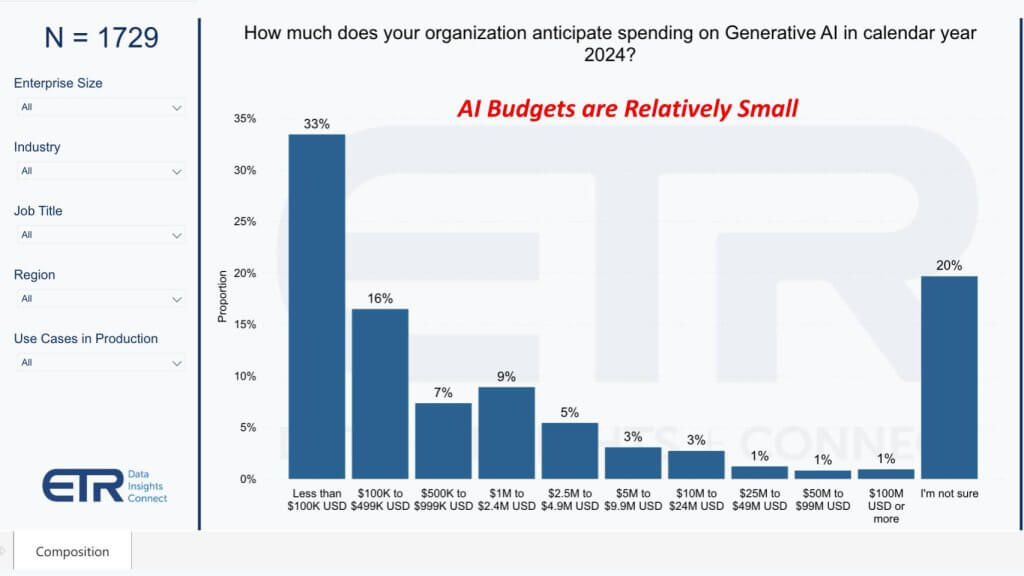

Let’s have a look at the AI finances distribution on this subsequent chart beneath. Right here ETR asks: How a lot does your group anticipate spending this yr on gen AI?

As you’ll be able to see above, the primary response, 33% of the 1,700-plus say lower than $100,000 yearly. That is fascinating since you see some large spenders out to the appropriate, spending $2.5 million to $5 million, $5 million to $10 million, and 6% of consumers spending greater than $10 million yearly. These large spenders skew the information and we’ll contact on that in a second. However typically, IT budgets allotted for AI are nonetheless comparatively small.

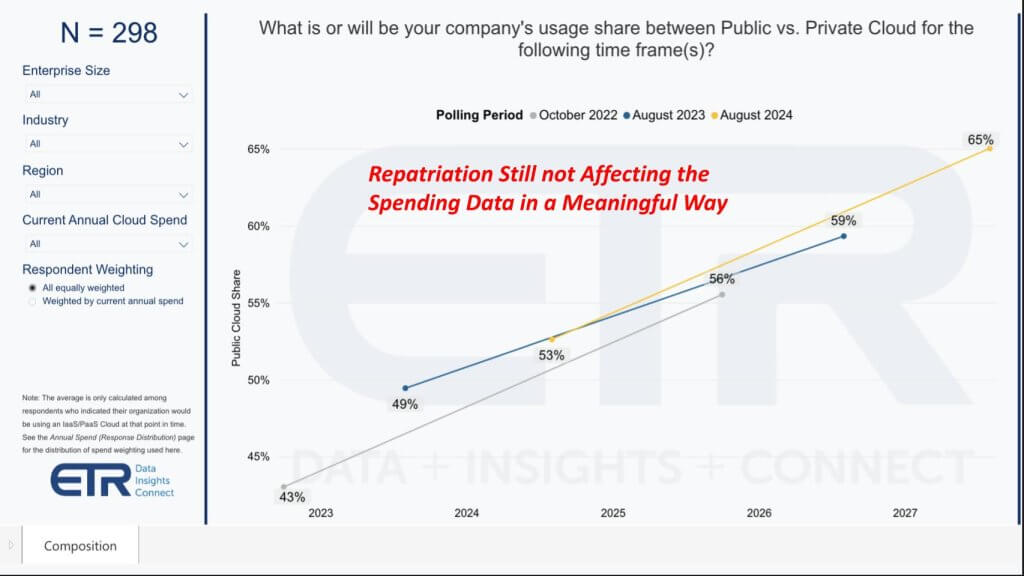

Cloud adoption continues to steadily advance… Repatriation nonetheless not thwarting cloud progress

Earlier than we dig into the AI spending skew, let’s check out some new information on cloud adoption. Under we present cloud adoption developments. ETR asks: What will likely be your organization’s utilization between private and non-private cloud for the next time frames?

Above we present information from three survey durations, October 2022 (grey line), August (blue line) and the latest October survey (yellow line). As you’ll be able to see, the cloud expectations proceed to enhance. It is a smaller pattern of 298 determination makers, however nonetheless, it’s significant.

Whereas we all know from anecdotal conversations that there’s undoubtedly some repatriation taking place, with clients complaining about value specifically. Nonetheless, it simply doesn’t present up within the macro numbers.

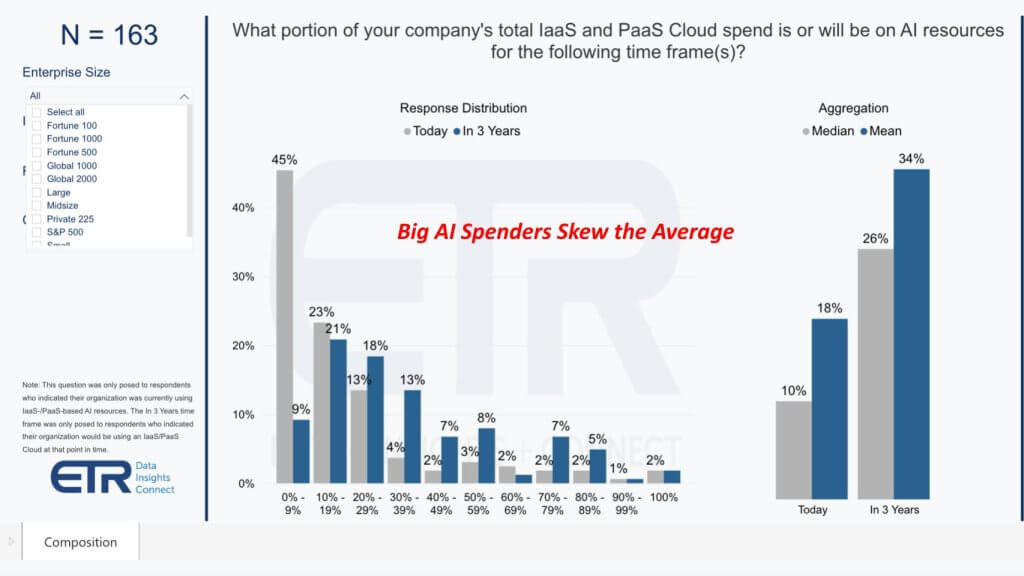

Cloud is prime to organizations’ AI plans however the ROI math continues to be elusive

Under we present the proportion of a agency’s whole cloud spend that’s being spent on AI assets. Once more, a smaller N, however this graphic reveals the distribution on AI. The grey is the median or midpoint and the blue is the imply or common.

Take a look at how the businesses leaning into AI skew the typical above. You possibly can see, for example, if you happen to have a look at the proportion that’s spending zero to 9%, the median is 45%. The imply drops right down to 9%, indicating that the large AI spenders skew the information. You possibly can see as you get to the rightmost parts of this chart, the 20% to 29% pops as much as 18% of the pattern and that’s the place the blue bar turns into dominant.

For those who go all the way in which to the far rightmost part of this chart, you’ll be able to see as we speak the median or midpoint is 10%, the imply is eighteen%, and that grows to 26% and 34%, respectively, three years out. Now, if you concentrate on the quantity of capital spending, the a whole lot of billions that’s being spent on AI proper now by hyperscaler cloud suppliers, and also you evaluate that to the cloud income, it’s a bit of scary in that the client expectations aren’t justifying the large cloud spend within the subsequent three years.

Take, for instance the large 4 cloud income of round $200 billion in 2024. And let’s say it’s going to develop inside three years to about $300 billion. If solely a 3rd of that’s actually going towards AI, you’re speaking about large numbers, $100 billion. However it pales into comparability with what’s going to be spent in that timeframe on the AI buildout. Now, the warning, I’d say, is that loads of that spend goes to be on embedded AI inside infrastructure, inside software program buried inside every kind of automation instruments. So the numbers might be a lot larger than our simple arithmetic suggests.

So it’s important to be a bit of bit cautious in decoding that information. However nonetheless, we want to see a bit of bit larger numbers because it pertains to that AI ROI.

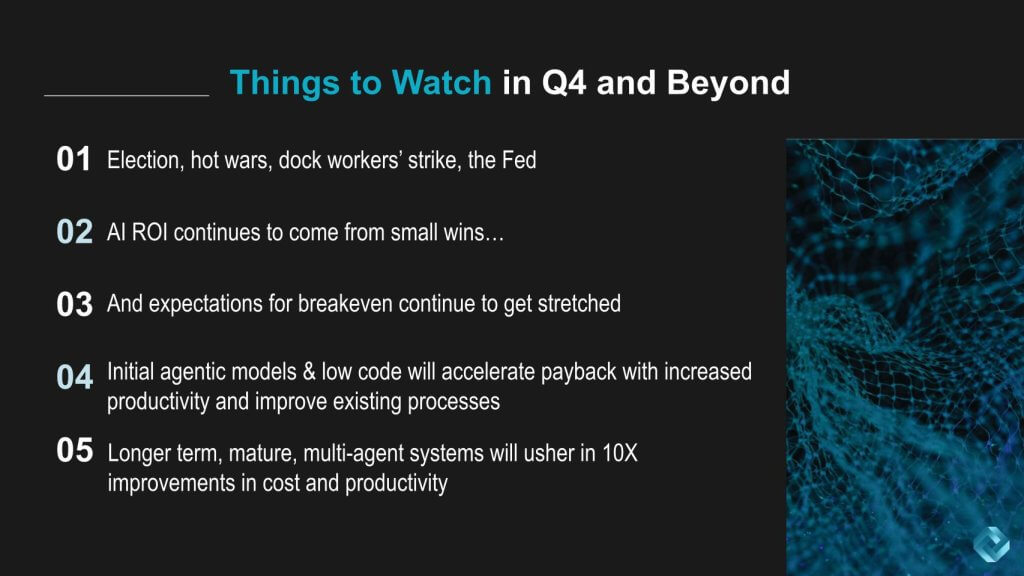

Issues to observe close to and much

Let’s have a look at the place we’re targeted in This autumn and past. We have now loads of exterior components occurring this yr. The election, at the least two scorching wars, doubtlessly three. The dockworkers strike appears to be settling, however we’ll see how that shakes out and its impression on inflation. There’s jobs reviews and finally the Fed’s actions on rates of interest, which has affected IT spending for the previous two years. Clearly these are issues are out of our management, however they’re undoubtedly vital components.

AI ROI, we prefer to say, is hitting singles. We’re not seeing the large big NPVs, or web current values. Lots of people get confused round ROI. They throw that time period round. In truth, it’s in all probability value speaking about it a bit of bit. So when you concentrate on, ROI it’s the share return on an funding. So consider ROI as a quite simple calculation. The ROI is profit over value.

So if you happen to can decrease the fee, the ROI will increase. That’s why so many chief monetary officers wish to decrease the fee, as a result of it lowers the denominator and will increase their return. However ROI is only a share. It doesn’t provide you with any indication of the dimensions of that return.

That’s why we like to have a look at the NPV and run a reduced money circulate. So what would you fairly have? Would you fairly have 100% ROI on a $100, or would you fairly have a one-Tenth the ROI on $1 billion? You see the distinction? Large share ROI with small returns, or small ROIs with large {dollars}.

Then there’s the idea of breakeven. Breakeven is the take after you place in all of the assets to get the venture began (that’s, the preliminary funding) to make your a refund. What’s that crossover timeframe?

On the fourth above, we’ve been speaking rather a lot about agentic fashions in AI going past a single agent or single copilots, and the preliminary agentic fashions that we’re seeing corresponding to these proven at Dreamforce. We’re going to see extra at Microsoft Ignite. Hopefully much more at Amazon Internet Companies re:Invent.

The preliminary fashions, together with low code, are going to speed up that payback interval with elevated productiveness and higher processes with present workflows. Typically, we discuss paving the cow path. It’s kind of a pejorative, but when we apply AI to present processes, that’s going to make issues higher. It’s an excellent flip of the crank, however it’s not going to provide you, if you happen to go to the final level on this slide, that 10X productiveness enchancment that our colleague David Floyer is all the time speaking about.

Longer-term, these mature multi-agent programs that we’ve been speaking about which have a harmonization layer and might connect with back-end legacy purposes that include loads of the information, the metadata, the enterprise logic and so forth. They will connect with these and have two-way interplay between the brokers and that harmonization layer, pushing updates into these back-end programs and in actual time trying on the digital illustration of a enterprise.

And really importantly, an agent management framework can allow these brokers to be ruled to work collectively in live performance, and interpret top-down objectives, top-down metrics and organizational aims to execute on a bottom-up final result. It’s vital to do not forget that that is going to take a very long time. That is years away earlier than we attain this nirvana. So within the meantime, we’re going to see an S-curve emerge.

And you understand what these appear to be. It takes some time to get issues going. And we’re within the flat a part of the S-curve proper now. Some individuals will name it the disillusionment interval. However actually they’re speaking about S-curves that haven’t but kicked in.

We’re excited, however we actually haven’t hit the steep a part of the curve. And when that occurs, for little or no effort, you get a giant return. That’s when everyone will get reignited. And so we actually suppose that that agentic framework that we’ve been placing forth has nice potential, and that’s one thing that we’re actually going to maintain doubling down on.

What do you suppose? What are you seeing for spending? What are you seeing when it comes to AI stealing from different budgets? What are you seeing for returns on the AI investments? Tell us.

Picture: theCUBE Analysis/DALL-E 3

Disclaimer: All statements made relating to corporations or securities are strictly beliefs, factors of view and opinions held by SiliconANGLE Media, Enterprise Expertise Analysis, different friends on theCUBE and visitor writers. Such statements aren’t suggestions by these people to purchase, promote or maintain any safety. The content material introduced doesn’t represent funding recommendation and shouldn’t be used as the idea for any funding determination. You and solely you might be liable for your funding choices.

Disclosure: Lots of the corporations cited in Breaking Evaluation are sponsors of theCUBE and/or shoppers of Wikibon. None of those corporations or different corporations have any editorial management over or superior viewing of what’s revealed in Breaking Evaluation.

Your vote of help is vital to us and it helps us hold the content material FREE.

One click on beneath helps our mission to supply free, deep, and related content material.

Be part of our group on YouTube

Be part of the group that features greater than 15,000 #CubeAlumni specialists, together with Amazon.com CEO Andy Jassy, Dell Applied sciences founder and CEO Michael Dell, Intel CEO Pat Gelsinger, and lots of extra luminaries and specialists.

THANK YOU