The Indian fairness market is on a excessive: once more. On August 1, Nifty 50, the benchmark index for the Indian fairness market, hit the ‘25000’ mark. The leap from 24000 to 25000 took simply 24 buying and selling classes.

By September 24, it soared previous ‘26000’. This unbridled bull run has, in truth, characterised the Indian fairness markets because the March 2020. Nevertheless, now the bullish frenzy has regulators involved.

On March 12, the Securities and Trade Board of India (SEBI) chairperson, Madhabi Puri Buch, underlined the ‘stretched valuations’ of small and mid-cap shares, iterating there are “pockets of froth” available in the market. On July 22, she shared her issues about speculative buying and selling in F&O phase and losses made by retail merchants on this phase.

Newest reviews recommend, SEBI is all set to tighten regulation to curb retail frenzy in fairness choices.

Are the issues of the regulator concerning a ‘froth’ available in the market legitimate?

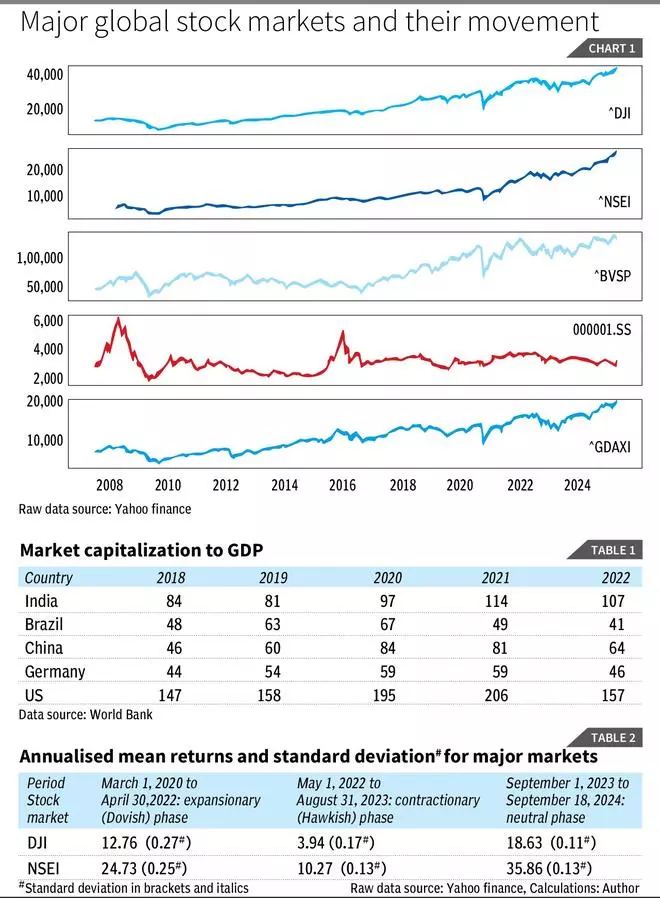

Chart 1 exhibits the six world markets: Nifty 50, India (NSEI), Dow Jones, United States (DJI), German Index (GDAXI), Bovespa Index, Brazil (BVSP), and SSE Composite Index, China (000001.SS) from 2015 to 2024.

For each market, we are able to see a pointy rally submit the pandemic, an unsure correction in 2022 and a sharper rally from late 2022 onwards. Nevertheless, for each DJI and Nifty 50 (prime two panels), the bullish spree within the final two years is awfully sturdy.

The market capitalisation (mcap) as proportion of GDP (Buffet indicator) suggests the Indian markets are overvalued. The Buffet indicator for India elevated considerably from 2019 to 2022, a sample which matches the US’ (Desk 1).

India’s mcap-to-GDP ratio reached a 15-year excessive of 140.2 per cent in Might 2024. Values of the Buffet indicator above 100 is, by itself, an indicator of overvaluation however with values skirting 150 per cent, the monetary sector has, it appears, determined to develop by itself. The issues of the regulator about ‘froth’ available in the market are evidently not unfounded.

What’s resulting in the continued bullish frenzy?

For one, the retail market contributors have entered the inventory markets in a giant approach submit Covid, particularly in India. Furthermore, there are issues that credit score progress in the actual sector may very well be discovering a path to the fairness market. Desk 2 presents the expansion within the US and Indian fairness markets throughout totally different financial coverage phases of the US Federal Reserve, broadly matched by central banks of main markets.

Expansionary part

The sharp rally in each the markets submit Covid coincides with the expansionary part. From Might 2022, Federal Reserve elevated rates of interest responding to inflationary pressures, resulting in some correction: for each DJI and Nifty 50, we see markets returns fall throughout contractionary part.

Nevertheless, with the speed hike paused from September 2023, the markets rallied sharply once more. With the Fed’s choice to slash rates of interest by 50 foundation factors in September 2024, we’re taking a look at one other expansionary part, which can stretch valuations on the upside.

How will the financialisation impression the actual economic system?

The signs of overvaluation convey forth issues about financialisation: proliferation of monetary belongings and monetary market progress unrelated to the actual sector progress.

First, financialisation makes corporations extra involved about ‘share-holder worth creation’ than actual capital accumulation. Financialisation can result in ‘distribute and disinvest’ slightly than ‘retain and reinvest’ for corporations, which is able to jeopardize the actual capital accumulation and employment technology.

Speculative surge

Second, the retail participation within the F&O phase and progress in intra-day buying and selling exhibits the inclination to make use of the fairness marketplace for speculative good points slightly than for long-term funding. This may be detrimental to retail contributors’ long-term saving behaviour, and adversely impression saving charges within the economic system.

Moreover, if the participation within the inventory market is leveraged, a market crash can result in substantial erosion of wealth for retail traders.

The Union Funds in 2024, elevated short-term capital good points tax (STCG) and launched a flat long-term capital good points tax (LTCG) throughout asset courses, discouraging short-term churning of portfolios. However have the market contributors, particularly the youthful retail merchants, taken the cue?

Going forward, regulatory measures mustn’t solely discourage leveraged buying and selling, but additionally create consciousness on acceptable danger administration methods for intra-day buying and selling and the pitfalls of shorter-term churning for long run monetary objectives. ‘Nudges’ could also be simpler than overt paternalism in guiding youthful retail contributors.

The author is Affiliate Professor at Nationwide Institute of Financial institution Administration, Pune. Views expressed are private