Two weeks in the past, Wall Road and retail buyers alike held their breath as Federal Reserve Chairman Jerome Powell took the stage on the Financial Symposium in Jackson Gap, Wyoming. Whereas the funding group listened to Powell’s each phrase, the next comment appears to have resonated nicely: “The time has come for coverage to regulate.”

I will exit on a limb right here and posit that the Fed is (lastly!) going to start lowering rates of interest. Such a change to financial coverage could be welcomed by many varieties of companies.

Specifically, I see fintech platform SoFi (NASDAQ: SOFI) as an apparent beneficiary of decrease rates of interest. An integral a part of Cathie Wooden’s Ark Make investments Administration portfolio, SoFi inventory has been decimated this yr. After cratering 26% thus far in 2024, SoFi shares at the moment commerce for simply $7.

Let’s dig into what is going on on with SoFi’s enterprise and assess how the corporate is so uncovered to rates of interest. With modifications to financial coverage wanting seemingly, now could possibly be a time to purchase the dip in SoFi inventory hand over fist.

Having a look at SoFi’s whole enterprise

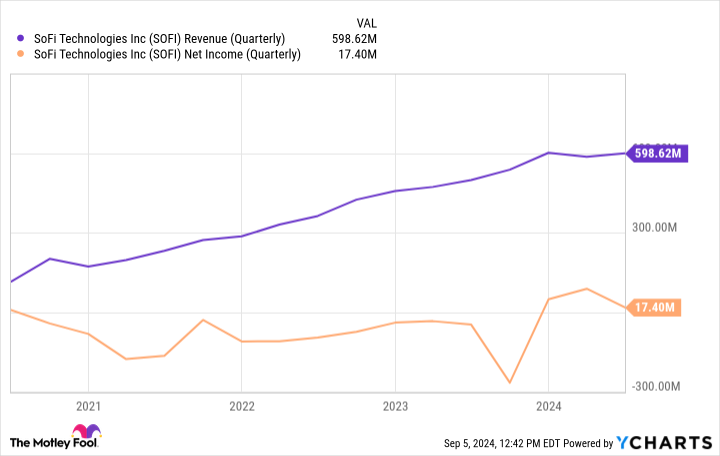

SoFi breaks its enterprise down into three main segments: lending, know-how, and monetary companies. Because the chart beneath signifies, SoFi has carried out a formidable job rising its income over the previous couple of years. Extra importantly, the corporate has additionally demonstrated that it is moved on from working losses and is on a path to generate persistently optimistic web revenue. Fairly good things, proper? Properly, possibly not.

Regardless of SoFi’s total relative power, there may be one blemish with the corporate’s operation. Lending companies is by far SoFi’s largest supply of progress. The issue is that the lending phase has proven noticeable deceleration all through 2024. For the six months ended June 30, SoFi’s lending enterprise generated a complete of $664 million in web income — solely a 3% enhance yr over yr.

I can see how slowing progress in an organization’s essential income would not bode nicely for investor confidence. I would warning buyers from hitting the panic button, although. There are nonetheless a few vital concepts to discover earlier than writing off SoFi’s prospects.

How would decrease charges affect SoFi?

Rising rates of interest do not simply make the price of capital dearer; they will even have a real ripple impact on the financial system at giant. Companies and customers could not be capable of entry loans at greater charges or will merely select to not get a mortgage even when their credit score meets a financial institution’s underwriting protocols. Contemplating SoFi’s largest enterprise is lending companies, it is not too shocking to see this phase come to a screeching halt throughout a interval of elevated rates of interest.

Nevertheless, given the latest remarks from Chairman Powell, I believe it is seemingly that the Fed goes to begin reducing charges quickly — and I am not alone on this prediction. Funding banks together with Goldman Sachs, Financial institution of America, JP Morgan, Wells Fargo, Morgan Stanley, and Citigroup are all forecasting a fee reduce in September.

Reducing charges might function a bellwether for lending companies. Because of this, I see a Fed fee reduce as a significant catalyst for SoFi and one that may assist supercharge the corporate’s efficiency. Particularly, I see refinancing in pupil loans and mortgages in addition to residence fairness loans as three use instances that might see some rejuvenated exercise for SoFi.

Now, though decrease charges ought to theoretically encourage an uptick in lending exercise, it is vital to evaluate the magnitude by which this dynamic impacts SoFi’s enterprise. Throughout the second-quarter earnings name, SoFi CEO Anthony Noto defined that when the financial system finally enters a decrease rate of interest atmosphere, SoFi will nonetheless “preserve a excessive fee relative to our competitors.” He went on to say that

as charges go down, the worth of our loans typically go up, all else equal, and so we are able to preserve a superior APY. That does not imply we could not change it. It simply means it will likely be superior to drive our differentiated worth proposition and leverage our aggressive benefit.

What Noto is saying is that even when charges come down, SoFi can preserve greater coupons relative to the competitors as a result of firm’s diversified platform, which affords customers a large number of financial-services merchandise — with lending being simply considered one of them. In his eyes, SoFi ought to witness an uptick in quantity in its lending enterprise whereas additionally sustaining robust unit economics regardless of lowered rates of interest.

Why now appears just like the time to load up on SoFi

One factor that I discover attention-grabbing about SoFi’s present buying and selling exercise is that the inventory has gone down throughout a interval when the corporate has transitioned from persistently burning money to having fun with a worthwhile enterprise. Furthermore, SoFi has managed to show constant earnings whereas its largest supply of progress (lending) has principally remained flat. A giant purpose for that is that the corporate’s technique to cross-sell different services and products all through its ecosystem is paying off in spades.

On the finish of June, SoFi boasted 8.8 million members on its platform — up 41% yr over yr. Amongst this consumer base, 12.8 million merchandise are being utilized. Because of this every SoFi member is utilizing 1.5 companies on common. This dynamic makes it simpler to maintain prices associated to buyer acquisition affordable, whereas concurrently attaining greater unit economics throughout your entire buyer base. Nonetheless, I do not assume buyers are absolutely appreciating this dynamic, they usually have gone as far as to punish SoFi within the type of heavy inventory sell-offs.

Contemplating fee cuts ought to encourage newfound exercise for lending companies at giant, I’d assume SoFi is in a reasonably stable place to witness much more accelerated progress throughout the highest and backside strains. In different phrases, I truly assume SoFi’s present profitability profile is kind of a bit beneath what it could possibly be as soon as the lending enterprise returns to regular progress ranges. I believe the enterprise is essentially misunderstood, and buyers are discounting the tailwind that fee cuts characterize for future progress. For all of those causes, I believe investing in SoFi proper now could be a no brainer.

Must you make investments $1,000 in SoFi Applied sciences proper now?

Before you purchase inventory in SoFi Applied sciences, contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the 10 greatest shares for buyers to purchase now… and SoFi Applied sciences wasn’t considered one of them. The ten shares that made the reduce might produce monster returns within the coming years.

Take into account when Nvidia made this record on April 15, 2005… in the event you invested $1,000 on the time of our suggestion, you’d have $630,099!*

Inventory Advisor gives buyers with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of September 9, 2024

JPMorgan Chase is an promoting accomplice of The Ascent, a Motley Idiot firm. Wells Fargo is an promoting accomplice of The Ascent, a Motley Idiot firm. Financial institution of America is an promoting accomplice of The Ascent, a Motley Idiot firm. Citigroup is an promoting accomplice of The Ascent, a Motley Idiot firm. Adam Spatacco has positions in SoFi Applied sciences. The Motley Idiot has positions in and recommends Financial institution of America, Goldman Sachs Group, and JPMorgan Chase. The Motley Idiot has a disclosure coverage.

Price Cuts Are Coming: 1 No-Brainer Cathie Wooden Fintech Inventory to Purchase Hand Over Fist Proper Now for Simply $7 was initially printed by The Motley Idiot